The challenges facing cities, from housing shortfalls to ageing infrastructure, competitiveness, climate change and migration to affordability, are well publicised. All the while, companies across the world are vying for skilled talent across a new landscape of both emerging technologies and the digitisation of traditional office-using sectors. City authorities are grappling with providing infrastructure to enable a step change in housing and commercial property development in an era of empty municipal coffers and heightened sovereign bond yields. Institutional owners are becoming more selective and risk-averse.

At the same time, pension funds – traditionally one of the largest institutional investors in the commercial real estate ecosystem – are undergoing substantial change in multiple major economies as the defined benefit (DB) model, which offers employees a pre-determined payout upon retirement directly managed by a fund, comes under strain. As a result, defined contribution (DC) funds are largely supplanting DB ones. These are characterised by a shift in the contribution and risk burden from the employer to the employee. Younger and higher-contributing employees generate larger levels of cash for investment over a longer horizon, while fund managers are less burdened by near-term payouts and can instead think more strategically and holistically.

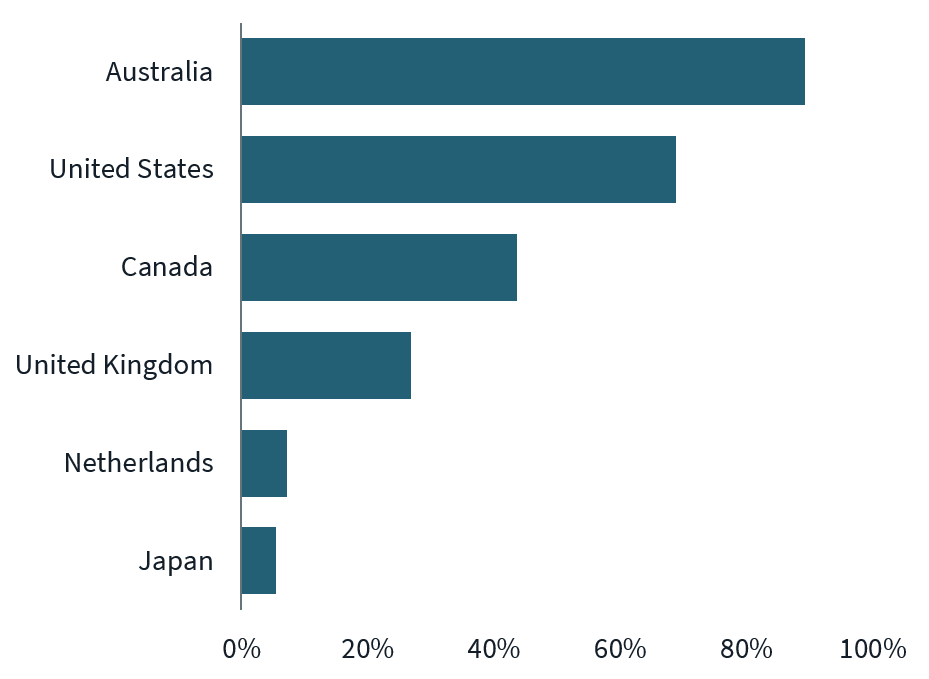

DC Shares by major country, JLL

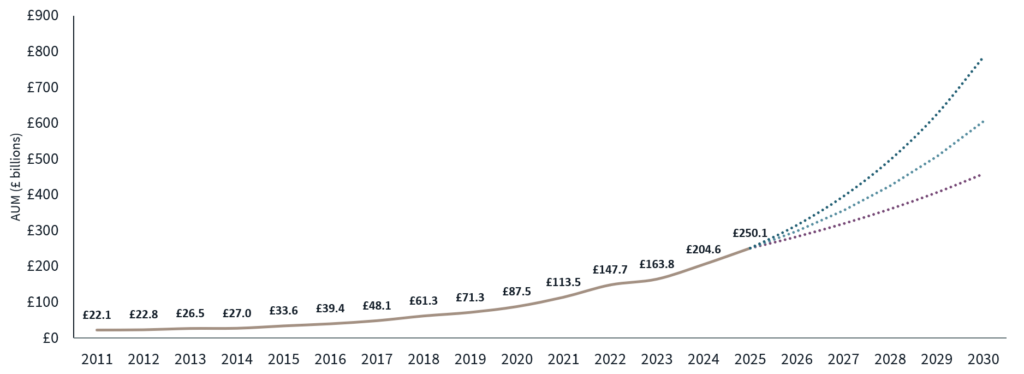

Assets under the purview of DC are growing at an exponential rate. This is also an uneven process, ranging from maturity in Australia and the United States above 70% take-up to only around 5% in Japan. This is about to change, and it will change fast. In the UK, the implementation of auto-enrolment has enabled DC funds to go from just £22.1 billion in AUM in 2011 to a staggering £250.1 billion in 2025. Future mandated consolidation of pension pots into “superfunds” alongside continuous compounding will bring this total to anywhere from £600 to £800 billion by the end of the decade.

Source: JLL Research, Pensions Regulator – UK DC schemes only, excludes hybrid schemes

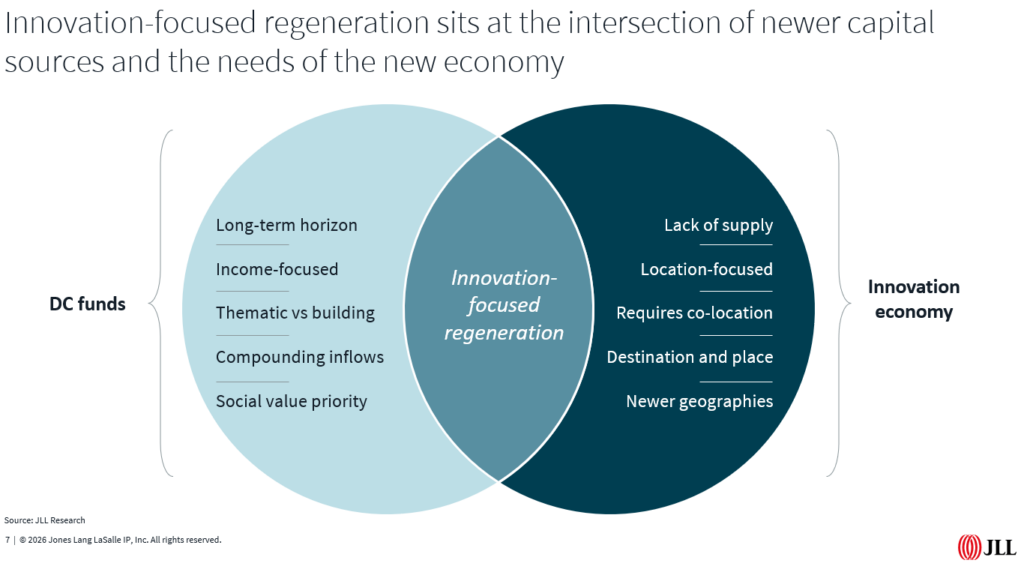

Meshing two opportunities

It may not be immediately obvious, but there’s an opportunity waiting in plain sight. DC funds need to interact in a highly complementary manner to innovative geographies. And these geographies require a wide array of investment and interventions to harness the power of deep talent pools. This capital is also needed for the co-location of research and educational institutions alongside government bodies and established corporate operations in experience-led clusters and locations.

The lack of supply of premium product for scaling AI, fintech and media firms intersects with a dearth of well located housing for employees. Improving place and experience is essential for creating differentiated clusters of specialisms but that can only happen if people can afford to be part of the journey.

Mixed use presents huge opportunity for UK towns and cities

Mixed-use regeneration allows all of this to occur at once over a long time horizon aimed at consistent income generation and “de-risking” across asset classes. This represents an attractive opportunity for DC funds approaching real estate investment from an thematic and LP perspective in partnership with developers, asset managers and public landholders rather than going building by building as a primary owner. The inclusion of affordable housing, community facilities and open space has the additional benefit of boosting social value.

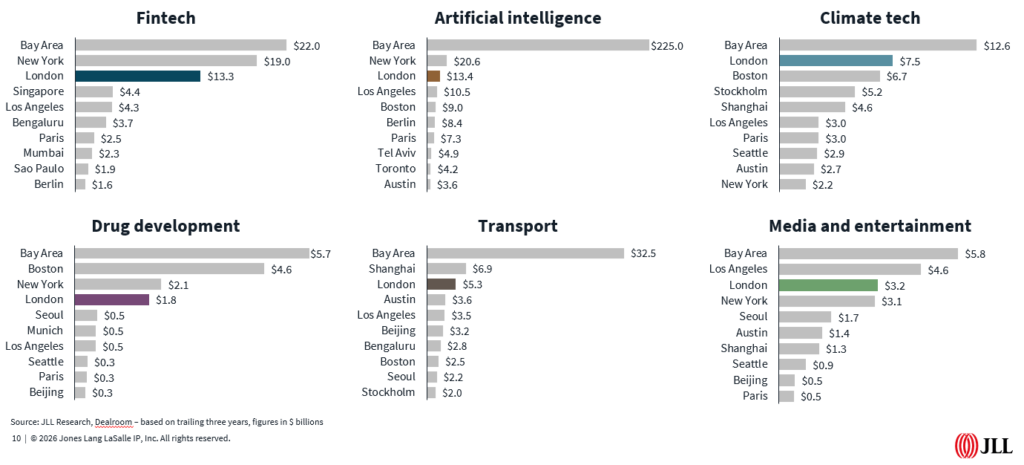

London stands in a unique position to capitalise on this shift. According to JLL’s 2026 edition of its Innovation Geographies reporting, London ranks third in the world after San Francisco and Boston for innovation, rising to second for its concentration of skilled talent. More broadly, the UK has attracted more venture capital than France and Germany combined for ten consecutive years, while London is a top-three destination for venture capital deployment in fintech, AI, climate tech, pharmaceutical development, transport and media.

However, this is not just about London. The UK has a range of key cities where single-digit vacancy is placing sustained upward pressure on rents as migration to smaller cities surges. The UK finds itself well placed to deliver growth across a range of key urban areas if it so chooses.

In Bristol, for instance, prime office rents now exceed £50 per square foot, with Edinburgh, Birmingham and Manchester not far behind. This is compounded by net internal migration to the eight largest regional innovation hubs in the country surging to nearly 520,000 people over the past three years and opening up a wide swath of additional regeneration opportunities. This will boost the momentum of big regeneration schemes such as Mayfield in Manchester, Smithfield in Birmingham and Brabazon in Bristol, amongst other. These quality propositions are well placed to take advantage of the forthcoming growth story.

Global leading cities as well as newer growth destinations alike can take advantage of alternative, longer-term and thematic investment strategies from entrants into the CRE sphere to create exciting, distinct and inclusive places and spaces. However, they will need to ensure a more flexible and permissive regulatory environment that can speed up and enable more consistency in the planning process. This needs to dovetail with bringing down the cost of building and the regulatory burdens associated with it. If they can, then the UK as a whole, not just London, can reap the benefits of the innovation economy, pension reform and demographic reshuffling.

Phil Ryan is the Senior Director of Cities Research, part of JLL’s Global Insight platform based out of London. In his role, he works with a variety of industry leaders ranging from developers to asset managers, pension and equity funds, city authorities and multinational corporates to translate the language of the built environment into strategies and advice for navigating a rapidly changing real estate landscape in cities around the world. He is a recognised leader in understanding the interaction between market fundamentals, city dynamics and long-term spatial planning and development trajectories and regularly speaks at conferences and events focusing on repairing and enhancing spaces and places.